How Much Income Do You Need to Buy a Home in San Diego?

Real Estate

Real Estate

Buying a home in San Diego is a dream for many, but with median home prices at $929,083 and housing costs 110–112% above the national average, understanding the income requirements is crucial before you start your search. Whether you're a first time buyer moving to San Diego or a local looking to upgrade, knowing exactly how much income you need to buy a home in San Diego helps you set realistic expectations and avoid financial stress.

In 2026, with mortgage rates expected to decline to 5.5–6.4% and 3–5% appreciation forecast, San Diego remains a competitive but attainable market for qualified buyers. Let's break down the numbers so you can determine if you're ready to make the move.

Before calculating income requirements, it's important to understand what you're buying into. The median home price in San Diego is $929,083, with most homes ranging from $880K to $1.1M. The average home value sits at $1,006,261, down 2.9% from last year, giving buyers more negotiating power. San Diego is forecast to see 3–5% appreciation in 2026, making it a solid long term investment.

Average rent is $3,059/month, with 1 bedroom apartments at $2,332/month, 2 bedrooms at $3,100–$3,156/month, and 3-bedrooms at $3,895–$4,778/month. Homes move quickly in San Diego, going pending in just 16 days on average, so buyers should get pre-approved and be ready to act fast. Property taxes average 0.64–0.67% annually, which comes to about $5,746/year on a median-priced home.

With inventory up 14.1% and 15.3% of listings having price cuts, 2026 offers more negotiating power than recent years.

When calculating how much income you need, don't just focus on the mortgage. San Diego's overall cost of living is 46–47% higher than the national average. Housing is 110–112% more expensive, utilities are 48–49% higher, and transportation is 42–43% above national norms. Groceries are about 11–13% higher, and healthcare is roughly 2% higher.

Beyond your mortgage, expect monthly expenses for a family of four to include groceries at ~$1,320/month, transportation at ~$401/month, utilities at ~$944/month, and healthcare at ~$788/month. Total monthly non-housing expenses are approximately $3,453/month for a family of four. Understanding these costs helps you budget realistically alongside your mortgage payment.

How does San Diego's income stack up against home prices? The average annual salary in San Diego is $72,237 ($34.73/hour). The median salary is $78,556, while the median household income reaches $104,321. Entry level positions start around $51,479, and top earners can make $117,274.

The gap between median household income ($104,321) and the income needed to afford the median home ($929,083) is significant, which is why many San Diego residents rent or live in more affordable nearby cities like Chula Vista, National City, or Oceanside.

To calculate income requirements, we use these assumptions: median home price of $929,083, 20% down payment ($185,817) to avoid PMI, loan amount of $743,266, mortgage rate of 6.0% (30-year fixed), property tax of 0.67% annually, homeowners insurance of ~$1,500/year, HOA fees of ~$300–$500/month, and a maximum debt-to-income ratio (DTI) of 43% for conventional loans.

Your monthly principal and interest payment would be approximately $4,460. Add property tax at ~$520/month, homeowners insurance at ~$125/month, and HOA fees at ~$300–$500/month, and your total monthly housing payment comes to ~$5,405–$5,605.

To keep housing costs at 43% or less of gross income, you need a monthly gross income of $12,802, which equals $153,624/year. However, financial advisors recommend keeping housing costs at 30% or less for a comfortable budget. At 30% DTI, you need a monthly gross income of $18,350, which equals $220,200/year.

For a $750,000 entry level home, you need approximately $124,000/year (43% DTI) or $178,000/year (30% DTI). For an $880,000 lower median home, you need $145,000/year (43% DTI) or $208,000/year (30% DTI). For the $929,083 median home, you need $154,000/year (43% DTI) or $220,000/year (30% DTI). For a $1,000,000 home, you need $165,000/year (43% DTI) or $236,000/year (30% DTI). For an $1,100,000 upper median home, you need $182,000/year (43% DTI) or $260,000/year (30% DTI).

Bottom line: To comfortably afford the median priced San Diego home at $929K, you need an annual income of $185,000–$220,000 with a 20% down payment.

Many buyers use FHA loans (3.5% down) or conventional loans (3–5% down). However, putting less down increases your monthly payment due to Private Mortgage Insurance (PMI).

With a 5% down payment on a $929,083 home, your down payment is $46,454, loan amount is $882,629, and PMI is ~$184/month. Your new monthly payment becomes ~$5,689 including PMI, requiring $159,000/year (43% DTI) or $227,000/year (30% DTI). The trade off is clear: lower down payment means higher monthly payment and higher income requirement.

San Diego offers several programs to help buyers with lower incomes. CalHFA (California Housing Finance Agency) offers down payment assistance up to 3.5% of loan amount with income limits and favorable interest rates. The San Diego County Homebuyers Program provides down payment and closing cost assistance targeted at first-time buyers and middle-income families, with income limits up to $137,500 for individuals and $157,000 for families.

Veterans Affairs (VA) Loans offer 0% down payment for eligible veterans with no PMI required and competitive interest rates. FHA Loans require just 3.5% down payment minimum with more lenient credit requirements (580+ FICO), making them ideal for buyers with $125,000–$150,000 income. These programs can reduce the income needed by $20,000–$40,000 annually, making homeownership more accessible.

San Diego's median home prices vary dramatically by neighborhood, and choosing the right area can significantly lower your income requirement.

More affordable neighborhoods include National City with median prices of $750K–$850K requiring $125,000–$170,000 income (43% DTI), Chula Vista at $850K–$900K requiring $140,000–$160,000, Linda Vista at $850K–$950K requiring $140,000–$165,000, and Clairemont at around $995K requiring $165,000+.

Mid-range neighborhoods include Mission Valley with median $667K requiring $110,000–$135,000, North Park at $875K–$950K requiring $145,000–$165,000, and Oceanside at $900K–$975K requiring $150,000–$170,000.

Luxury neighborhoods require significantly higher income. La Jolla has a median of $2.2M+ requiring $400,000+ income, Del Mar at $2.5M+ requiring $450,000+, and Poway at $1.1M+ requiring $185,000+.

Pro tip: If your income is under $150,000, focus on National City, Chula Vista, Linda Vista, or Mission Valley for better affordability.

Understanding San Diego's job market helps you gauge whether your income aligns with local housing costs. Healthcare employers include UC San Diego Health, Sharp HealthCare, Scripps Health, Rady Children's Hospital with salaries ranging from $70,000–$150,000+. Biotech companies like Illumina, Dexcom, Neurocrine, Halozyme pay $90,000–$200,000+. Defense employers including General Atomics, Northrop Grumman, U.S. Navy offer $75,000–$180,000+. Technology companies like Qualcomm, Cisco, ServiceNow pay $85,000–$220,000+. Education employers at UC San Diego, San Diego State University offer $60,000–$140,000+.

Healthcare and biotech added 17,000+ jobs recently, making these sectors the most stable for buyers.

Get pre-approved first to know your exact budget before browsing. Lenders will tell you exactly what you qualify for based on your income, debts, and credit score.

Save for a larger down payment since every extra percent down reduces your monthly payment and PMI costs. Aim for 10–20% if possible.

Consider first-time buyer programs like CalHFA, San Diego County programs, and VA loans, which can reduce your income requirement significantly.

Look at emerging neighborhoods like Linda Vista, Clairemont, and Chula Vista, which offer more affordable entry points while still providing great schools and amenities.

Factor in all costs including property taxes (0.64–0.67%), HOA fees ($300–$500/month), insurance, and maintenance (1% of home value annually).

Work with a local expert like Heritage Homes RE, which specializes in helping buyers find homes for sale in San Diego that fit their budget, including off-market deals and neighborhoods with strong value.

Consider buying now since mortgage rates are expected to drop to 5.5–6.4%, inventory is up 14.1%, and 15.3% of listings have price cuts, making 2026 a favorable year to buy.

San Diego's median household income is $104,321, but affording the median home ($929K) typically requires $185,000–$220,000 annually. This gap means many buyers rent first while saving for a larger down payment, buy in more affordable nearby cities like Chula Vista or National City, partner with a co-buyer to combine incomes, use first-time buyer programs to reduce requirements, or wait for mortgage rates to drop further in 2026.

If your income is under $125,000, consider renting while saving or looking at nearby cities like Chula Vista or Oceanside where median prices are lower.

Understanding how much income you need to buy a home in San Diego is the first step toward homeownership. With median home prices at $929K, you'll typically need $185,000–$220,000 annually for comfortable affordability, but first-time buyer programs, lower-priced neighborhoods, and strategic down payments can make this goal more achievable.

Heritage Homes RE is your trusted local partner for a free affordability consultation to determine your exact budget, finding homes for sale in San Diego that match your income, connecting you with lenders and first-time buyer programs, accessing off-market deals and expert market analysis, and guiding you through neighborhoods from La Jolla to Chula Vista.

Contact Heritage Homes RE today for a free homebuying consultation. Let us help you determine if you're ready to buy and find the perfect home in your budget.

📞 Call or text us or visit

to get started.

To buy the median-priced San Diego home at $929,083, you need an annual income of approximately $185,000–$220,000 with a 20% down payment. For a $1M home, expect to need $200,000+ annually for comfortable affordability.

The average salary in San Diego is $72,237 per year ($34.73/hour). The median household income is $104,321, and the median salary is $78,556.

Yes. San Diego's cost of living is 46–47% higher than the national average. Housing is 110–112% more expensive, utilities are 48–49% higher, and transportation is 42–43% above national norms.

The median home price is $929,083, with most homes ranging from $880K to $1.1M. The average home value is $1,006,261.

With $100,000 income, you can afford a home priced around $550,000–$650,000 (depending on debts and down payment). This limits you to Mission Valley or nearby cities like Chula Vista or National City. Consider first-time buyer programs to increase affordability.

20% down ($185,817 for median home) avoids PMI and lowers monthly payments. However, FHA loans (3.5% down) and conventional loans (3–5% down) are available. VA loans offer 0% down for eligible veterans.

Most affordable: National City ($750K–$850K), Chula Vista ($850K–$900K), Linda Vista ($850K–$950K). Mid-range: Mission Valley ($667K), North Park ($875K–$950K), Oceanside ($900K–$975K).

Yes. CalHFA offers down payment assistance up to 3.5%. San Diego County Homebuyers Program assists first-time buyers with income up to $137,500–$157,000. VA loans offer 0% down for veterans.

Mortgage rates are forecast to decline to 5.5–6.4% in 2026, down from current ~6.1%. Fannie Mae predicts 6.2%, while Morgan Stanley expects 5.50–5.75% by mid-2026.

Yes. Mortgage rates are expected to drop, inventory is up 14.1%, 15.3% of listings have price cuts, and 3–5% appreciation is forecast. The market is the most balanced in almost a decade.

Stay up to date on the latest real estate trends.

Real Estate

Kimberly Koll

A practical guide to home affordability, income requirements, and the best neighborhoods for buyers in San Diego

Real Estate

Simple, high impact steps to help your home sell faster and for more in San Diego’s competitive market

Real Estate

Kimberly Koll

How to Afford, Find, and Close on Your First Home in America’s Finest City

Real Estate

Kimberly Koll

Explore expert predictions for home prices, mortgage rates, inventory levels, and the top San Diego neighborhoods expected to thrive in 2027.

Real Estate

Kimberly Koll

A Complete Guide to Home Affordability in San Diego's High Cost Market

Real Estate

Kimberly Koll

Browse, Compare, and Find Your Dream Home Faster with These Essential Mobile Tools

Real Estate

Kimberly Koll

Perfect Weather, Top Rated Schools, and a Thriving Job Market Make San Diego a Top Relocation Destination

Real Estate

Kimberly Koll

Expert Analysis on Mortgage Rates, Home Price Forecasts, and San Diego Market Opportunities

San Diego

Kimberly Koll

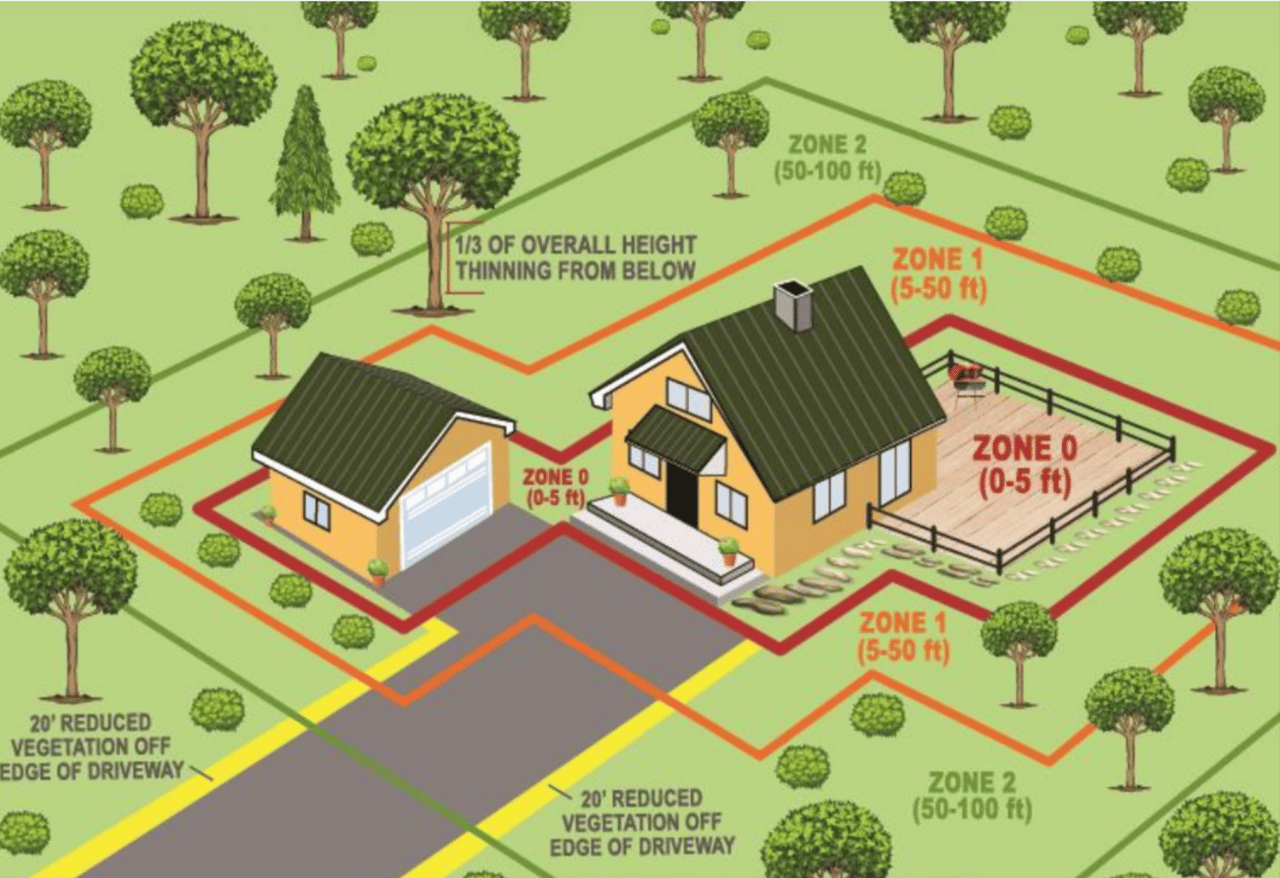

New Wildfire Defensible Space Regulations Protect Your Home and Property Value

Get in Touch

You’ve got questions and we can’t wait to answer them.

Get In Touch

HERITAGE HOMES SAN DIEGO

Kimberly Koll | DRE# 01506747

CONTACT

ADDRESS

16776 Bernardo Center Dr, #110D

San Diego, CA 92128